United States Cheese Market Size and Forecast 2026–2034

Rising Demand, Premium Innovation, and Steady Growth Shape America’s Expanding Cheese Industry

The United States cheese market is entering a period of steady and sustainable growth, supported by evolving consumer preferences, expanding premium segments, and strong distribution networks. According to industry estimates, the United States Cheese Market is expected to reach US$ 56.75 billion by 2034, up from US$ 41.53 billion in 2025, registering a CAGR of 3.53% from 2026 to 2034.

This growth trajectory reflects more than just rising consumption—it highlights a transformation in how Americans view cheese: from a traditional kitchen staple to a versatile, premium, and health-conscious product category. With innovation accelerating across natural, processed, and specialty segments, the industry is positioning itself for long-term expansion.

United States Cheese Industry Overview

The United States cheese industry stands among the largest and most diversified globally, underpinned by the country’s advanced dairy infrastructure and strong domestic appetite for cheese-based foods. Production is concentrated in key states such as Wisconsin, California, New York, and Idaho, each contributing significantly to the national output.

Cheddar, mozzarella, American, and Swiss varieties dominate mainstream consumption. However, specialty and artisanal cheeses are rapidly gaining ground, especially among consumers seeking unique flavors, organic sourcing, and premium culinary experiences.

The U.S. dairy ecosystem benefits from:

Advanced dairy farming practices

Modern automated processing facilities

Cold chain logistics infrastructure

Strong retail and foodservice distribution networks

Cheese consumption continues to grow steadily due to its versatility in traditional meals, quick-service restaurant (QSR) offerings, snacks, ready-to-eat foods, and gourmet cooking applications. Whether melted on pizza, layered in sandwiches, or enjoyed as a standalone snack, cheese remains deeply embedded in American food culture.

Market Segmentation

The U.S. cheese market is segmented by type, product, distribution channel, and geography.

By Type

Animal-Based

Plant-Based

While animal-based cheese remains dominant, plant-based alternatives are expanding due to vegan and lactose-intolerant consumers.

By Product

Mozzarella

Cheddar

Parmesan

Ricotta

Cream Cheese

Others

Mozzarella and cheddar account for the largest volume share due to widespread household and foodservice usage.

By Distribution Channel

Hypermarket/Supermarket

Convenience Stores

Online

Others

The rapid expansion of online grocery platforms and direct-to-consumer models is reshaping purchasing behavior.

Top States Driving Demand

California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, New Jersey, Washington, North Carolina, Massachusetts, Virginia, Michigan, Maryland, Colorado, Tennessee, Indiana, Arizona, Minnesota, Wisconsin, Missouri, Connecticut, South Carolina, Oregon, Louisiana, Alabama, Kentucky, and the Rest of the United States.

Growth Drivers in the United States Cheese Market

1. Rising Domestic Consumption and Changing Food Habits

Cheese consumption in the United States has consistently increased, supported by shifting lifestyles and convenience-driven eating habits. As Americans embrace ready-to-eat meals, quick snacks, and food delivery services, cheese plays a central role in product formulation.

The growing popularity of:

Pizza and burgers

Sandwiches and wraps

Pasta dishes

Snack kits and protein packs

Meal kits and frozen meals

has significantly boosted cheese demand. Millennials and Gen Z consumers are especially experimental, exploring international cuisines and gourmet varieties. This behavior has widened the market beyond traditional cheddar and mozzarella toward brie, goat cheese, and flavored blends.

Additionally, cheese is increasingly positioned as a high-protein snack, aligning with health-focused diets. Portion-controlled packs and resealable packaging further enhance convenience.

2. Expansion of Specialty and Artisanal Cheese Segments

Premiumization is a major theme in the U.S. cheese market. Consumers are increasingly willing to pay more for organic, locally sourced, hormone-free, and handcrafted products.

Specialty cheeses such as:

Goat cheese

Blue cheese

Brie

Lactose-free varieties

Organic and grass-fed options

are seeing strong growth among urban and higher-income consumers.

Farmers’ markets, gourmet retailers, and specialty online platforms have enhanced visibility for artisanal producers. Retailers are also investing in sampling campaigns and pairing suggestions (wine and cheese combinations), further stimulating demand.

As consumer awareness grows, specialty and artisanal segments are expected to contribute significantly to revenue growth over the forecast period.

3. Technological Advancements and Supply Chain Efficiency

Technology is reshaping cheese production and distribution. Automation in dairy plants reduces operational costs and improves scalability, allowing producers to maintain consistent quality while meeting rising demand.

Key innovations include:

Advanced pasteurization techniques

Improved fermentation processes

Vacuum-sealed and resealable packaging

Portion-controlled formats

Cold chain optimization

Digital supply chain management tools are improving demand forecasting and inventory management. These efficiencies reduce waste and enhance shelf life, particularly important in nationwide distribution.

Such advancements are helping manufacturers compete effectively in a highly competitive environment.

Challenges Facing the Market

1. Fluctuating Milk Prices and Raw Material Costs

Milk is the primary input in cheese manufacturing, and price volatility remains a persistent challenge. Factors influencing milk prices include:

Seasonal production cycles

Feed costs

Weather conditions

Government dairy policies

Rising costs of packaging materials, labor, and energy further strain profit margins. Large manufacturers may hedge against volatility, but smaller artisanal producers often face greater financial risk.

Managing input cost fluctuations while maintaining competitive retail pricing remains a balancing act for industry players.

2. Health Concerns and Changing Dietary Preferences

Health awareness continues to influence consumer choices. Concerns about high fat, sodium, and cholesterol levels in certain cheese products are prompting some consumers to reduce intake.

Simultaneously, plant-based alternatives made from nuts, soy, or other non-dairy ingredients are gaining attention. Veganism and lactose intolerance trends are creating competitive pressure.

To adapt, manufacturers are introducing:

Reduced-fat options

Low-sodium formulations

Lactose-free variants

Clean-label products with minimal ingredients

Transparency in sourcing and ethical dairy farming practices are becoming increasingly important to consumers.

Recent Developments in the U.S. Cheese Market

Innovation remains central to competitive positioning. Several key product launches in 2025 illustrate the market’s dynamic nature.

In June 2025, Tillamook introduced four new summer cheeses: Spicy Mexican Blend and Extra Sharp Cheddar shreds, along with Spicy Colby Jack and Smoked Medium Cheddar slices. These products cater to bold flavor preferences and convenience-driven cooking.

In May 2025, Belle Chevre launched innovative goat cheese products, including Señor Cactus Dips and CHEVOO Labneh Mediterranean-style spreads, emphasizing global flavors and premium positioning.

In March 2025, Sargento introduced snackable Shareables trays in collaboration with Mondelez International, as well as Seasoned Shreds featuring McCormick hot sauce flavors and Natural American Cheese with just five ingredients—highlighting clean-label appeal and portability.

These launches demonstrate how brands are responding to evolving tastes, portability needs, and flavor innovation trends.

Competitive Landscape

The U.S. cheese market features a mix of multinational corporations and regional producers. Major players include:

Land O’Lakes

Saputo Inc.

Arla Foods amba

The Kraft Heinz Company

Royal FrieslandCampina N.V.

Glanbia Plc

Savencia Fromage & Dairy

All companies are analyzed from five viewpoints:

Overview

Key Persons

Recent Developments

SWOT Analysis

Revenue Analysis

Competition revolves around pricing strategies, brand recognition, innovation pipelines, sustainability initiatives, and distribution expansion.

Outlook Through 2034

With a projected market value of US$ 56.75 billion by 2034, the United States cheese market is positioned for steady expansion. Growth will likely be driven by:

Rising snacking culture

Expansion of premium and specialty varieties

Clean-label and health-focused innovations

E-commerce and omnichannel retail growth

Export opportunities

While challenges such as milk price volatility and plant-based competition persist, the resilience of domestic demand provides a strong foundation.

Final Thoughts

The United States cheese market is not merely expanding—it is evolving. From traditional household staples to gourmet offerings and protein-rich snack innovations, cheese continues to adapt to modern dietary patterns and consumer expectations.

Backed by a strong dairy infrastructure, technological innovation, and steady domestic consumption, the market’s forecast growth to US$ 56.75 billion by 2034 reflects confidence in long-term demand stability. As brands balance health trends, sustainability, and premiumization, the U.S. cheese industry is poised to remain a cornerstone of the broader food and beverage sector for years to come.

About the Creator

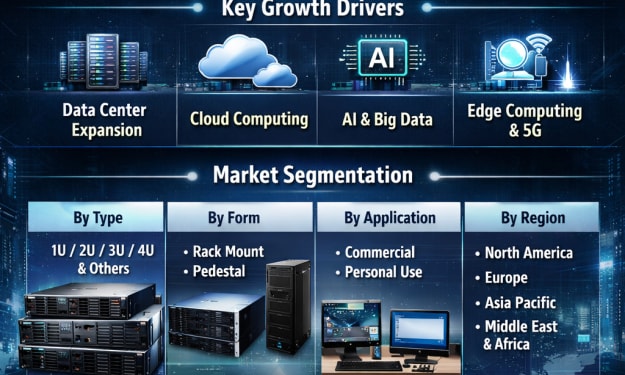

Server Chassis Market Size & Forecast 2026–2034

The Server Chassis Market is projected to grow from US$ 372.43 billion in 2025 to US$ 488.92 billion in 2034, expanding at a CAGR of 3.07% from 2026 through 2034. The steady rise reflects sustained investments in hyperscale data centers, cloud computing infrastructure, artificial intelligence (AI) workloads, and edge computing networks.

By shibansh kumar3 days ago in Trader

Australia Smart Safety Helmets Market 2026: Workplace Safety Innovation, Connected Protection and Industry 4.0 Integration

Australia Smart Safety Helmets Market Overview Australia’s smart safety helmets market is rapidly emerging as workplaces adopt advanced safety solutions that integrate digital technology with traditional protective gear. Smart safety helmets — equipped with sensors, communication modules and IoT connectivity — provide enhanced protection, real-time monitoring and automation support across construction, mining, manufacturing and industrial environments. As businesses prioritise employee safety, operational efficiency and compliance with stringent occupational standards, smart safety helmets are increasingly recognised as crucial components of modern safety ecosystems.

By Amyra Singha day ago in Trader

Unofficial Challenge: Black History Celebration

Forward: February 28th, 10:53 PM, EST... The final hour of Black History Month, 2026. Hello fellow writers. I've had this challenge waiting in my drafts for most of the month. But I held off on publishing it, until now.

By Sam Spinelli3 days ago in Writers

Comments

There are no comments for this story

Be the first to respond and start the conversation.